I’ve spent a lot of time diving deep into tax-advantaged accounts over the last 12 months. Roth IRA, Solo 401k, Mega Backdoor Roth — I’ve written about all of them. But, there’s one account that stands above them all when it comes to pure tax efficiency. The three magic letters are HSA or a Health Savings Account. And here’s what drives me crazy: most people who have access to one are completely misusing it. They treat it like a checking account for medical expenses. They get the debit card, swipe it at the pharmacy, and call it a day. This strategy leaves a lot of value on the table! An HSA isn’t really a healthcare spending account. If you know how to use it right, it’s potentially one of the most powerful wealth-building tool the IRS has ever created. Let’s dive in:

The Triple Tax Advantage of an HSA (That’s Actually Quadruple)

You’ve probably heard people talk about the “triple tax advantage” of HSAs. Here’s what that actually means: 1. Tax-deductible contributions When you contribute to an HSA, you get a tax deduction. This directly reduces your taxable income for the year. For 2026, you can contribute up to $4,400 if you have individual coverage or $8,750 for family coverage. If you’re 55 or older, you can add another $1,000 on top of that. 2. Tax-free growth Unlike a regular brokerage account where you pay taxes on dividends and capital gains, everything inside your HSA grows completely tax-free. You can invest in stocks, bonds, mutual funds, ETFs or whatever your HSA provider allows and owe no taxes on the gains. 3. Tax-free withdrawals When you take money out for qualified medical expenses, there are zero taxes. No income tax. No capital gains tax. Nothing. This combination is unique in the entire tax code. A traditional 401k gives you #1 and #2, but you pay taxes when you withdraw. A Roth IRA gives you #2 and #3, but you don’t get a deduction going in. Only the HSA gives you all three. But wait – there’s actually a fourth tax advantage that nobody talks about. 4. FICA tax savings (the secret fourth advantage) If you contribute to your HSA through payroll deduction at work, those contributions are exempt from Social Security and Medicare taxes (FICA). That’s an extra 7.65% savings that you literally cannot get with any other account. This makes HSA contributions through payroll the single most tax-efficient way to save money in America. Let me show you the math: If you’re in the 24% federal bracket and pay 5% state tax, plus the 7.65% FICA savings, you’re effectively getting a 36.65% discount on every dollar you contribute. Put another way: for every $1,000 you put in your HSA, it only “costs” you about $634 in after-tax dollars.

The Age 65 Bonus

Here’s another feature that makes HSAs incredible for long-term planning: Once you turn 65, you can withdraw money from your HSA for any reason without penalty. You’ll pay ordinary income tax on non-medical withdrawals (just like a traditional IRA), but there’s no 20% penalty. Before 65, if you withdraw for non-medical expenses, you pay income tax PLUS a 20% penalty. Ouch. After 65, it’s just income tax. This means your HSA effectively becomes a backup retirement account. Use it for medical expenses tax-free, or use it for anything else and pay regular income tax. And unlike a 401k or traditional IRA, HSAs have no required minimum distributions. You can let the money grow tax-free as long as you want.

How Most People Use Their HSA (Wrong)

Here’s what I see most people do: They contribute to their HSA, get the debit card, and immediately spend every dollar on medical expenses throughout the year. This isn’t terrible — you’re still getting the tax deduction and tax-free spending. That’s valuable. But you’re leaving an enormous amount of money on the table. The real power of an HSA comes from letting it compound for decades. And the IRS has created a loophole that makes this possible.

The Shoebox Strategy

Here’s the thing most people miss: there is no deadline for HSA reimbursements. If you pay $1,000 for a medical expense today out of your own pocket, you can reimburse yourself from your HSA… whenever you want. Tomorrow. Next year. In 30 years. The IRS doesn’t care. As long as you:

- Had the HSA open when you incurred the expense

- Keep the receipt

- Haven’t already claimed a tax deduction for that expense

You can reimburse yourself at any point in the future, completely tax-free. This is called the “shoebox strategy” because you could theoretically keep all your medical receipts in a shoebox and cash them in decades later. Here’s how to actually use this: Step 1: Pay for medical expenses out of pocket (ideally with a credit card so you get the points too) Step 2: Save all your receipts somewhere digital – scan them, photograph them, whatever works Step 3: Max out your HSA contributions and invest the money Step 4: Let it compound for years or even decades Step 5: Whenever you need cash for anything, reimburse yourself from your HSA using old receipts The money comes out tax-free because it’s technically reimbursement for medical expenses. But since you paid those expenses years ago, you’re effectively turning your HSA into a flexible savings account with tax-free investment growth. Let me give you a specific example: Let’s say you spend $2,000 per year on out-of-pocket medical expenses: co-pays, prescriptions, glasses, dental work, whatever. Over 20 years, that’s $40,000 worth of receipts sitting in your digital filing system. Meanwhile, you’ve been maxing out your HSA every year. At $8,550 for family coverage, invested in index funds averaging 8% annual returns, your HSA could grow to over $400,000. When you need money — for a vacation, a down payment, anything — you pull up those old receipts and withdraw $40,000 completely tax-free. This is genuinely one of the craziest loopholes in the entire tax code. And it’s completely legal.

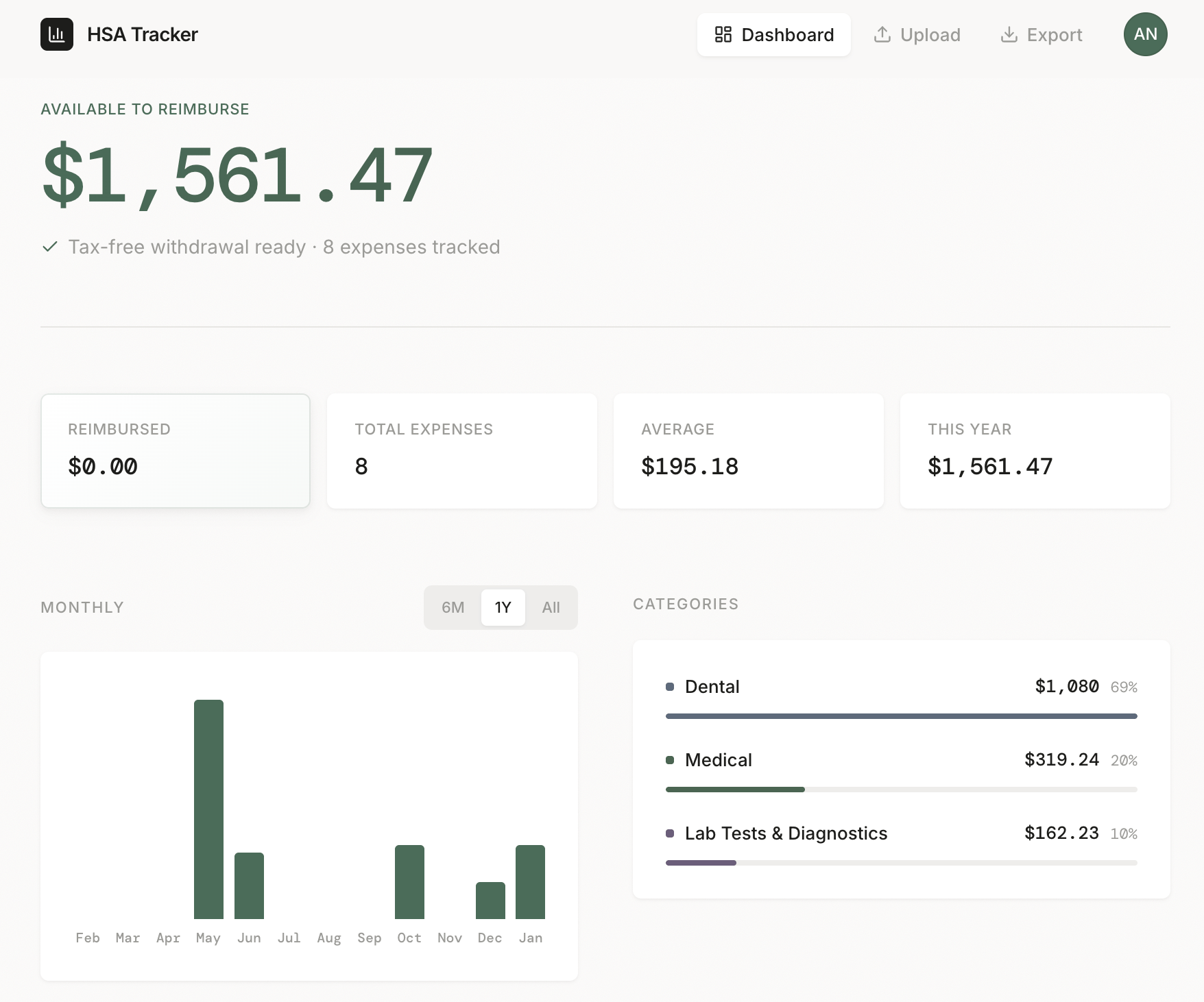

Free Tool for Tracking HSA Expenses

The Silly Money team built a free HSA Tracker tool to make it incredibly easy to keep track of your out-of-pocket expenses.

I used to use a Google Sheet until our team built this and it’s been a significant upgrade since:

- AI image recognition to make receipt tracking and entry super easy

- Tracking for a whole family including the ability to attribute expenses to individual family members

- The ability to download my data as a CSV and ZIP is helpful for peace of mind

And it’s a much sleeker interface that makes keeping track of reimbursements so much easier. Check out the free HSA Tracker here

Is a HDHP Worth It?

The catch with HSAs is you need to be enrolled in a High-Deductible Health Plan (HDHP) to contribute. For 2026, that means a plan with:

- Minimum deductible of $1,700 (individual) or $3,400 (family)

- Maximum out-of-pocket of $8,500 (individual) or $17,000 (family)

A lot of people are scared of HDHPs because of the word “high deductible.” But here’s how I think about it: The math usually works in your favor. HDHPs typically have significantly lower premiums than traditional plans. The premium savings alone often cover the difference in deductibles… and then some. And when you factor in the HSA tax advantages, HDHPs quite often win out. Let’s run some quick numbers: Let’s say switching to an HDHP saves you $200/month in premiums. That’s $2,400/year in your pocket. If you put that $2,400 into your HSA and you’re in a combined 35% tax bracket, you’re saving another $840 in taxes. So you’re actually $3,240 ahead before you even consider the investment growth or the FICA savings. Yes, you’ll pay more out of pocket if you have a major medical event. But the premium savings plus tax advantages typically outweigh the risk for most reasonably healthy people. The exception: If you have predictable, significant medical expenses (chronic conditions, planned surgeries, pregnancy), a traditional plan might make more sense. But for most people? The HDHP + HSA combo wins.

HSA vs FSA

If your employer offers a Flexible Spending Account (FSA), you might wonder how it compares to an HSA. Short answer: an HSA wins almost every way you look at it. And the word “Flexible” in an FSA is incredibly ironic as the account is anything but. Here’s the full breakdown:

| Feature | HSA | FSA |

|---|---|---|

| 2026 Contribution Limit | $4,400 / $8,750 | $3,400 |

| Rollover | Unlimited, forever | Limited ($680 max) or lose it |

| Investment options | Yes | No |

| Portability | Yours forever | Tied to employer |

| Ownership | You own it | Employer owns it |

The “use it or lose it” rule with FSAs is brutal. If you don’t spend the money by year-end (or within a short grace period), it’s gone. With an HSA, your money is yours forever. Change jobs? Keep your HSA. Retire? Keep your HSA. It follows you for life. The one advantage of FSAs: you don’t need an HDHP. So if you’re on a traditional health plan, an FSA is your only option. But if you have a high-deductible health plan? HSA every time.

My HSA Strategy

Here’s what I personally do:

- Max out contributions every year: I contribute the full limit through the year.

- Pay medical expenses out of pocket: I use a credit card for the points and keep digital copies of all receipts.

- Invest aggressively: Since I’m not touching this money for decades, I keep it in growth-oriented investments.

- Track expenses religiously: I use HSA Tracker to log every qualified medical expense with the date, amount, and receipt location.

- Let it compound: The plan is to let this grow for 20-30 years, building up both investment value AND reimbursable expenses.

Eventually, I’ll have a massive pool of tax-free money I can access whenever I want by pulling up old receipts. It’s like a Roth IRA with an escape hatch.

Conclusion

If you have access to an HSA and you’re not maxing it out, you’re leaving serious money on the table. It’s the only account in America with true triple (really, quadruple) tax advantages. It’s portable, investable, and has no expiration date. The shoebox strategy turns it from a simple medical spending account into a flexible wealth-building tool that beats almost every other option available. If your employer offers an HDHP with HSA access, seriously consider it. Run the numbers on premium savings plus tax advantages. For most healthy people, it’s a no-brainer. And if you’re self-employed, you can set one up yourself… there’s no employer required. Start stacking those receipts. Your future self will thank you. What did you think of this article? Reply and let me know.

P.S. One of my most read articles on Silly Money is where I break down how to get the highest return from your cash. I’m teaching a free workshop on Thursday called How to Maximize Your Earnings on Cash where I break down:

- Money‑Market Funds 101 – what they are, how they stay liquid, and why yields keep rising.

- Tax‑Smart Variants – funds that can sidestep state or federal taxes.

- Tax‑Equivalent Yield – the quick formula to compare apples to apples.

- Picking the Winner – a simple filter for the fund that leaves you with the most money in your pocket.

- Automated Options – see how certain platforms can automate the whole play for you.

Sign up here I’ll also send a replay to everyone who registers!

Author Disclosure: I’m writing this as myself, not as some investment adviser or broker-dealer. I’m not a tax professional, this is all purely educational or my personal thoughts – not investment, legal, tax, or professional advice. Financial decisions involve risk, including losing money. Taxes are complex. Please do your own research or talk to a licensed pro before acting on anything you read here.