One of the most interesting quirks of the US tax code: If you earn over $150,000 single, or $236,000 as a married couple, you cannot directly contribute to a Roth IRA. But, you can use the “Mega Backdoor Roth” to fund your Roth IRA with up to $70,000 every single year! I brought in my CPA friend Bogdan from The Crunch to write this article to break down:

-

What the Mega Backdoor Roth is

-

Who can qualify to use this loophole

-

A step-by-step process to take advantage of this

-

How to report this correctly in your tax forms

Over to him!

What is the Mega Backdoor Roth?

The Mega Backdoor Roth is a strategy that allows you to contribute significantly more to Roth accounts than the standard annual limits. For example, if you are a high W-2 earner, and are:

-

Maxing out your Roth IRA account (through a Backdoor Roth IRA)

-

Maxing out your Traditional 401(k) contribution of $23,500 per year

-

Receiving a $10,000 employer match.

This strategy allows you to contribute up to an additional $36,500 to a Roth account. This is calculated as the annual 401(k) limit ($70,000) minus the maximum traditional 401(k) contribution ($23,500) and any employer match (in this example, $10,000) The contribution limit increases further as you approach retirement age:

-

If you are age 50 to 59 or 64 or older, you are eligible for an additional $7,500 in catch up contributions, which increases the total to $77,500.

-

If you are between the ages of 60 and 63, you get an additional $11,250 in “super catch-up contributions” which increases the total to $82,250.

This table makes it easier to visualize your limits:

|

Age |

Employee Contribution Limit |

Total 401(k) Limit (max mega backdoor limit) |

|---|---|---|

|

Under 50 |

$23,500 |

$70,000 |

|

50-59 |

$30,500 |

$77,500 |

|

60-63 |

$34,750 |

$82,250 |

|

64 or older |

$30,500 |

$77,500 |

This strategy could be a great way to get as much money as possible into a Roth account (where money grows entirely tax-free) before investing additional amounts in your taxable brokerage.

How the Mega Backdoor Roth Works

This strategy is only available through your 401(k) retirement plan. You need to either have:

-

An employer whose 401(k) plan allows for after-tax contributions. You can check with HR if this is supported.

-

Self-employment income or a side hustle that qualifies you for a Solo 401(k).

A quick way to verify whether your employer 401(k) supports this feature is to log into your 401(k) provider’s site and view the available options:

Look for the “after-tax’ option.

If you see the “After-tax” option, it means you are able to do the Mega Backdoor Roth! Here are some popular companies that offer the Mega Backdoor Roth:

-

Google

-

Amazon

-

Meta

-

Apple

-

Stripe

-

Netflix

What about business owners?

If you are a small business owner with no-full time employees excluding your spouse, you can set up a Solo 401(k) plan that supports this feature. The big brokerages do not support this since its requires more administrative work on their end. However, you can use providers like Carry that will let you set up a Solo 401(k) plan that supports an automatic mega backdoor conversion. If you have a full-time W-2 job that does not support the mega backdoor Roth, but earn some income on the side with a side hustle, you can still do a Solo 401(k) for your side hustle!

Step-by-Step Mega Backdoor Roth Guide

The Mega Backdoor Roth is a two step process:

-

Step 1: You first contribute to a 401(k) after-tax account (don’t confuse it with the Roth 401(k))

-

Step 2: You can then roll the funds over to the Roth IRA or Roth 401(k), depending on your plan options.

I recommend checking your “Summary Plan Description” to ensure that you understand your options, the rollover process (i.e. Roth IRA vs Roth 401(k)) and other relevant details. Why would someone do this?

-

Enables large contributions to a Roth account (up to $70,000 annually).

-

All growth afterwards is tax free.

-

Protected from creditors under ERISA. If the company goes bankrupt, your dollars are still safe.

What are some of the disadvantages?

-

Additional paperwork. You will receive 1099-R for the rollover and potentially another one for the gains. Some accountants/CPAs may not be familiar with the Mega Backdoor Roth. Be prepared to explain the strategy or learn how to report it accurately if you prepare your own taxes.

-

If the company fails the nondiscrimination test (rare, but possible), the plan has 2 ½ months to correct excess contributions. This is why you rarely see smaller businesses offering it, but it should be safe at larger employers.

Roth IRA vs Roth 401(k)

Step 2 requires you to roll the after-tax contribution into either a Roth 401(k) or a Roth IRA. Is one option better than the other? Double check that your plan document allows for both options — some plans exclusively allow you to roll it into a Roth 401(k) account. But if you have both options available, here are the benefits of each:

-

Roth 401(k) – It could minimize your taxable earnings with automatic conversion and potentially be easier to set up.

-

Roth IRA – This typically supports more investment options and has more flexible withdrawals (can withdraw contributions penalty-free at any time)

In my opinion, rolling into a Roth IRA is a better option due to flexibility, but a Roth 401(k) works well too.

Dealing with Earnings

When you contribute to an after-tax account (step 1), the amount is usually automatically invested. Then, when you roll the balance into a Roth IRA (step 2), you may have some earnings. These earnings are taxable income. To reduce this taxable amount, do steps 1 and 2 as soon as possible. Occasionally, you may get lucky and find a plan provider that has an automatic rollover to minimize any earnings (like the Carry Solo 401(k)), but most plans do not. Some employers may issue separate checks to split contributions and earnings. If that happens, you could put the after-tax contributions into a Roth IRA and the earnings into a Traditional IRA to avoid paying taxes. Important: Contributing to a Traditional IRA can significantly complicate or negate the benefits of a Backdoor Roth IRA due to the pro-rata rule. The Backdoor Roth IRA is an entirely separate loophole from the Mega Backdoor Roth, but most people like the option to do both!

Example

Say you have $5,000 in your Roth IRA and contribute $10,000 to the after-tax 401(k) account (step 1). You then roll it into a Roth IRA (step 2). Assume there was $100 in earnings between steps 1 and 2. You then have two options:

-

Option 1: You can roll $10,100 into the Roth IRA and pay taxes on the $100 of earnings. Your total Roth IRA account will be $15,100

-

Option 2: Roll over $100 into the Traditional IRA (no tax impact) and roll over $10,000 into the Roth IRA. Your total Roth IRA account will be $15,000. You need to check your plan to ensure that you can split them into two checks if you decide to go with the latter option.

While both options work, Option 2, which involves paying taxes on the earnings, is generally the cleaner and simpler long-term solution.

Tax Reporting for the Mega Backdoor Roth

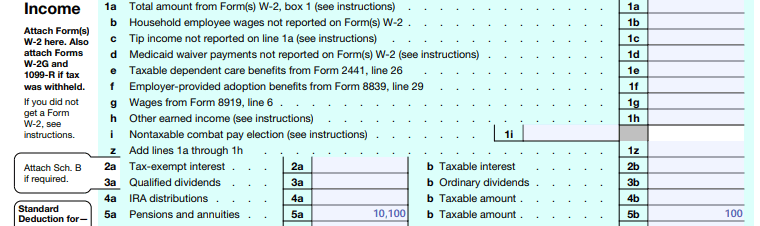

At the end of the year, you will receive a 1099-R form that you will need to report on your taxes. On your Tax Form 1040, Line 5a (Total IRA Distributions) will show $10,100, and Line 5b (Taxable amount) will show $100.

Double check with your tax preparer!

If you rolled $10,000 into a Roth and $100 into a Traditional IRA, Line 5b will be $0, with no tax impact. If you are using a tax preparer, tell them exactly what you did so they can report it correctly. You can always look at Form 1040, Line 5 to double-check if they did it right.

Thanks for reading! If you made it this far, I have a favor to ask: I’m currently redesigning the newsletter website and looking to add a few reader testimonials. If you are enjoying Silly Money, reply with 1 sentence on what you love about it, and I’ll feature the best responses on the new homepage!